In our last Saphineia Insight, The Six-Million-Dollar-Man, we discussed the value creation opportunity at middle market Food & Beverage manufacturers from enhancing procurement practices.

Inventory control is the opposite side of this same coin. For the same reason that there’s a lot of money at stake in procurement (ie, materials costs typically represent 50%-60% of a manufacturer’s revenue), there is significant risk associated with not managing inventory effectively.

The events described below are true. Names have been changed to protect the confidentiality of those involved.

Elizabeth, 30-years-old, had just graduated from a prominent business school and was excited to

join the investment team of Strongbow Capital, a well-regarded PE firm that invests in the Food

& Beverage manufacturing sector.

Shortly after starting in June, Elizabeth was assigned to work on the platform acquisition of a

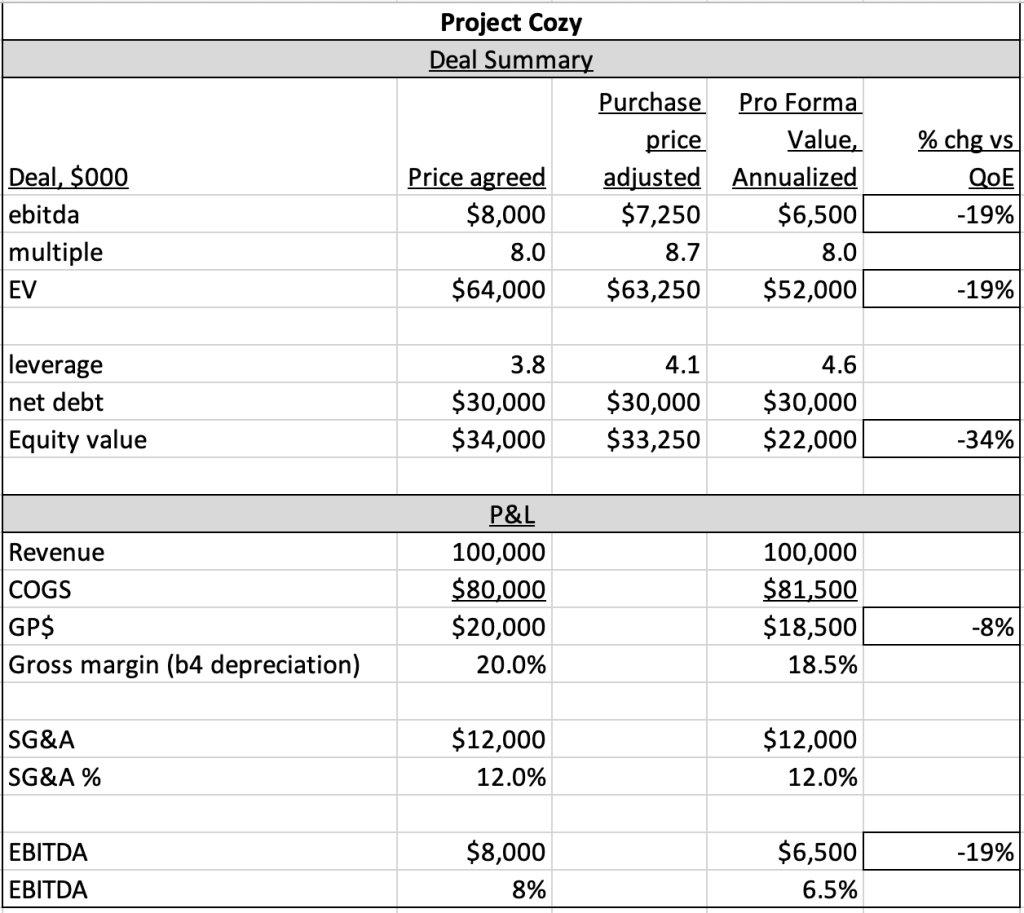

$100mn soup maker. Diligence on the deal, code-named ‘Project Cozy’, was well-underway,

with closing scheduled in 2 weeks. One of the closing conditions was a physical inventory count

to validate the value of inventory on Cozy’s balance sheet.

Over the course of 2 days, Elizabeth watched as multiple teams, each consisting of 2 of Cozy’s hourly employees, walked the aisles of the 60,000 square foot warehouse, clipboards in hand, counting and recording the results of their counts. Periodically, they brought their count sheets into a conference room, where Cozy’s finance department input the results into its ERP system. Progress was slow, as Cozy had high turnover among its hourly employees, and many of the counters had little familiarity with the physical inventory process generally and Cozy’s warehouse specifically as most served in production roles.

Further, many of the counters had just a high-school education and calculation challenges quickly emerged relating to the proper unit of measure (i.e., in some instances, the correct measure was cases; in others it was pounds or even eaches), requiring re-counts. Compounding matters, the facility had just 4 functioning forklifts, so the counting teams spent much of their time waiting for an available forklift.

Not surprisingly, the counters and Cozy’s management quickly became frustrated. Management’s frustration was heightened as production and shipments were paused during the count and late delivery was already a pain-point for Cozy’s customers.

The Results

Finally, all pallet positions had been counted. However, when Cozy’s finance team compared the ERP with the counts, it discovered extremely large discrepancies in multiple inventory items, necessitating additional recounts. Several counters were sent home while Cozy’s finance department (and Elizabeth) stayed and performed the recounts themselves.

Finally, at 3:00 a.m., the recounts were completed and results finalized: Cozy’s inventory had been overstated by $750,000! Per the acquisition agreement, the purchase was reduced by a like amount.

At least the deal closed and, Elizabeth thought, we now can go about executing our value-creation-plan.

The Forensic Audit

Unfortunately, this wasn’t the end of the story. Six months later, following the completion of Cozy’s fiscal year, Strongbow’s auditor required another physical inventory given the results of the June count. Lo and behold, another six-figure inventory adjustment was needed.

This time, Strongbow was ticked off. A giant shouting match ensued with the sellers’ CEO and CFO, both of whom had remained with the business post-acquisition. Strongbow’s Board of Directors instructed it to hire a forensic accounting firm to study the root causes of Cozy’s inventory inaccuracies.

One month later, the firm’s findings came back. Its conclusions were deeply troubling:

- Approximately 10% of Cozy’s inventory had been received into inventory without a Certificate of Analysis, which meant that Cozy didn’t know when some of its raw material inventory had been manufactured – and thus when it expired!

- Cozy’s warehouse employees did not consistently scan inventory to the correct location upon receipt – due in part to high employee turnover in the warehouse and limited training programs for new hires.

- Warehouse employees regularly ignored basic, “First Expired-First-Out” picking practices, resulting in a high level of expired raw materials and finished goods.

- Cozy did not accurately capture in-process scrap during the production process (e.g., damage, overfill, spills, out-of-spec).

- While Cozy’s R&D capabilities consistently delivered excellent top-line growth, its sales teams regularly over-estimated demand for new offerings – leading to high product obsolescence and write-offs of labels, finished goods and raw materials unique to these FG items.

- Lastly, inventory write-offs were not a new problem for Cozy, as large write-offs had been taken following previous physical counts.

Lessons Learned

For Elizabeth, this was quite an introduction to manufacturing and the importance of sound inventory control practices, highlighting the following:

- Due to its poor inventory control practices, Cozy had over-stated EBITDA by nearly 20%, as the cost of purchased materials were often not recognized in the appropriate accounting period.

- Cozy’s realized inventory loss rate greatly exceeded the scrap assumptions in its product costing model.

- Cozy’s inventory write-offs should not have been added back to EBITDA as these ‘losses’ were real and recurring cash expenses.

- Lastly and most importantly, her firm had dramatically overpaid for Cozy.

Conclusion

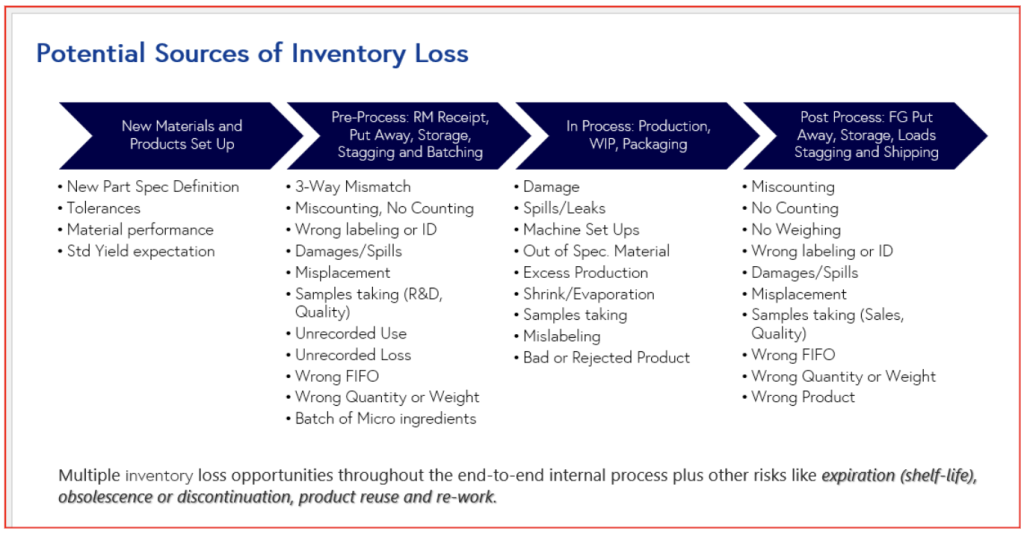

Unfortunately, Elizabeth’s experience with Cozy is not unusual in the middle market. Inventory losses are often hard to spot and track as they can occur anywhere along the manufacturing process, from item set-up to material receipt and ultimately through the shipment of finished goods (see below).

As a result, many middle-market Food & Beverage manufacturers are leaving profits on the shop floor. The good news is such losses are identifiable, estimable and correctable.